If you want to learn how to start a real estate brokerage in 2022, you could do worse than learn from Jeff. Jeff (not his real name) was a Brooklyn kid who managed to grow a literal mom-and-pop brokerage in Williamsburg into a small empire he sold to NRT for a reported mid-eight figure.

Now, you might be thinking that Jeff was lucky. That he started at the low end of the market and rode one of the largest upswings in New York City real estate history all the way to F#$&* You money. You’d be right, of course, but you’d also be missing the point.

To paraphrase a wise man I once knew, you can only fish with the rod you’ve got. You can’t create the market, but you can learn how to start a real estate business that will easily enable you to 10x your gross commission income (GCI) by 2022. Here’s how to get started.

1. Before You Even Think About Starting a Brokerage, Find Your Why

Before you even think about starting a real estate brokerage, you need to understand that 80-hour weeks will become your new normal, and chances are better than average that you’re going to fail. If you do, you might find yourself back where you started with an extra $50,000 (or more) in debt. But failing is OK. Failure = growth.

Why You Should Trust My Advice

In my 27 years in the real estate industry, I’ve been a REALTOR 30 Under 30 agent, broker-owner, franchise partner, recruiter, speaker, coach, and author. I’ve launched two brokerages, invested in two more, and coached dozens of broker-owners. I’ve already put in the 80+ hour weeks, made it through the sleepless nights, bought the Porsche, the boat, and yes, I made mistakes along the way. Lots of them.

That’s why I decided to write this guide. I want you to learn from the mistakes I made and build a sustainable brokerage from the ground up. In order to do that, you need to start from the principles.

7 Things I Wish I Knew Before Starting My Real Estate Brokerage

Why Do You Even Want Your Own Real Estate Business?

If you’re going to bring your A-game and function at your best every single day, you’re going to need motivation. I hate to say it, but unless you’re Lex Luthor, money won’t be enough. After all, you’re living comfortably now, right? Do you really think you’ll be able to wake up ready to go every single morning if all you’re after is money?

✋ Money Is Not Enough to Fuel Your Daily Grind

If you really want to succeed, you’re going to have to dig a little deeper than money as a source of motivation. You might even ask yourself, “Why do I want money in the first place?” While that may seem obvious at first, it gets murkier the more you think about it. Why do you want to be rich?

Maybe you really crave independence or want to prove something to yourself or a loved one. Maybe you have a family that you desperately want to provide for. Whatever your reason, you better know what it is before you get started. Unless, of course, you want to wake up in a cold sweat nine months from now and realize you want to work in a nonprofit, write books, teach kids, or a million other less painful journeys and don’t really care about money at all.

“He who has a why can suffer any how” — Friedrich Nietzsche

Study after study has shown that in order to be successful at a difficult task, your goals need to be concrete rather than wishful thinking. So if you want to have the motivation to get you well out of your comfort zone every day, you need to figure out what you want in as much detail as possible. Once you have your target, you’ll be surprised at how much energy you have to actually get there.

It All Starts With Your MVV (Mission, Vision & Values)

In order to create the motivation to keep going that inspires you more than money, you need to sit down with your partners and come up with a heartfelt Mission (why you’re doing it), Vision (what it looks like when you achieve it), and Values (what ideals, standards, and rules you will follow to achieve it) statement. While this may seem a little woo-woo, it’s actually a crucial first step for building a successful business. Every decision you make, every agent you recruit, and how people see your brokerage in the market will be based on your MVV.

[Related article: How to Create an Inspiring Mission, Vision & Values for Your Brokerage]

2. Figure Out If You & Your Partners Are Qualified to Start a Brokerage

Before you start doing anything else, you need to take the time to figure out if you and the partners you plan to work with are qualified to run a real estate business. Here’s a quick checklist to make sure everyone on your team is ready to hit the ground running.

Do You Have a Broker’s License or Can You Hire a Broker of Record?

While this one might seem obvious, you’d be surprised at how many people who have zero real estate experience want to set up shop in hot markets. Legally, of course, you’re going to need at least one person on your team to have their broker’s license so they can be the broker of record—aka the person legally responsible for all the transactions any agent in your brokerage completes.

In some states, like New York, you can also hire a broker of record to take on that responsibility for you. While this might seem like an ideal solution in theory, in practice it can be a bit of a nightmare. Many brokers for hire want to just sign their name for a fee and basically never show up at the office.

I call these brokers “Four-star Generals.” Since they think they have “earned their stripes,” they’re entitled to just sit behind a desk and bark orders. This strategy makes it much harder to grow a sustainable business.

Do You Have Enough Savings to Live for at Least a Year With No Income?

This is an important one. Even if you have the perfect plan and the money in the bank to make it work, you can never really predict success in your first year. The market might shift, the economy might tank, or your partners might abandon you. That means you need to mitigate the risk of going bankrupt by having enough savings to last you for at least a year without income. Like Warren Buffet said, “Don’t risk what you have and need for what you don’t have and don’t need.”

Do You Trust Your Partners?

Whenever money is involved, even the best of friendships can become strained. So before you start planning your brokerage with other people, ask yourself if you really trust them. Are they professional? Do they have enough money in the bank to not make rash decisions because they need quick cash? There is no shortcut to vetting your partners, so make sure you get to know them well before you even think about planning your brokerage.

It is unlikely that two or more people will be in consensus 100% of the time and this will lead to strife and indecision, so beware. Both can kill your business and possibly your friendships too.

In a successful business operating agreement, there is usually one person who is ultimately in charge of making the final decisions. It is important to decide now who that person is and how others will handle it when decisions don’t go their way.

Can You or Your Partners Get Financing?

If you’re new to business ownership, you might be surprised to learn that even billionaires use loans to finance new businesses. There’s a simple formula to understand why: OPM > YM. That is, using other people’s money is better than using YOUR money. This is a concept popularized by Robert Kiyosaki, and it’s popular for a reason. It works.

Depending on the type of brokerage you want to start and where you want to start it, you could be looking at $10,000 to $250,000 in capital to get started. For example, to start a virtual brokerage, you just need to:

- Incorporate your business

- Get errors and omissions (E&O) insurance

- Acquire voice-over-internet-protocol (VoIP) software and phones

- Purchase some basic lead generation and transaction management software

- Choose a good customer relationship management (CRM) tool (or even better, an all-in-one platform that can scale with your growth), and start recruiting agents.

That means that $10,000 might be enough to bootstrap your business.

If you want to start a brick-and-mortar real estate business, well, all bets are off. If you’re in a big city, you will be looking at renting office space for $2,500 to $7,000 per month for a small office in a good location. You can double that for a high-traffic storefront in New York City or San Francisco. You’ll also need to secure a long-term lease and pay for furniture, computers, Wi-Fi, and other utilities. Instead of that $10,000 bootstrap budget, you might need to budget $10,000 per month.

So look into potential sources of finance you and your team can acquire quickly and cheaply. Small Business Administration (SBA) loans are a popular choice as they take money from your 401(k) to start your business. You can also look at traditional business loans or personal loans from family or friends.

Tell us about you so we know what to send.

3. Start Building Your Dream Brokerage (on Paper)

Once you’ve spent enough time honing in on your why, it’s time to start working on the how by outlining the steps you need to take to reach your goal. In this stage of starting a real estate brokerage, you will actually start building your brokerage on paper. It’s also the perfect time to run through the potential problems that may arise before you write that first rent check.

What Kind of Brokerage Would Make You Happy?

Before you run any numbers, spend a few hours trying to figure out what kind of brokerage would make you happy to run five years from now. Is it a large brokerage? A small boutique brokerage that focuses on luxury properties? Or would you rather work with investors and focus on property management and fix and flip? What kinds of people do you want to work with? What office culture would make you excited to come to work every morning?

It’s important to not worry about money here, so just try to focus on what you want and flesh it out on paper in as much detail as you can. Next, we’ll take your dream brokerage and see how it stacks up against your local market.

Would It Make More Sense to Just Buy a Franchise?

Before you sink your life savings into a new brokerage, you might want to consider investing in a franchise. Franchises have a few compelling advantages:

Franchises Come With an Established Brand

This is nothing to sneeze at. Many franchises like Keller Williams have spent millions of dollars and invested decades into building brands that the public, and the agents you’re going to try to recruit, already trust.

Franchises Come With Processes, Software & Support

Instead of reinventing the wheel, you can buy your way into an established real estate business with the processes, software, and support that will help de-risk your brokerage.

Franchises Can Be Easier to Sell

When you decide to ride off into the sunset like Jeff, a franchise will be much easier to sell than a boutique brokerage.

However, franchises also have some serious disadvantages:

Franchises Come With Rules That Limit Your Creativity

If you’re not willing to cede creative control over your brand and business, owning a franchise may not be for you.

Most Good Territories Are Already Taken

The fact that you can buy your way into a turnkey real estate business isn’t exactly a secret. Most, if not all, of the good territories available in your city might already be taken.

Ask Sean: Should I Buy a Franchise or Start My Own Brokerage?

Is There Room for Your Dream Brokerage in Your City?

By now you should know what will motivate you, you’ve vetted partners, and you have some ideas about what kind of brokerage will make you happy. The next step in starting a real estate business is to figure out if your dream brokerage fits into your local market.

This stage can be extremely time-consuming in large cities, or might take an afternoon of work in a smaller town you know well. In order to find out whether or not your dream brokerage makes sense for your area, look at the current successful brokerages, see what they’re doing right—and more importantly, what they’re doing wrong that you could do better.

Here are some things you should look for:

1. Listings

Are the listings in your local area split relatively evenly between brokerages or is there one dominant brokerage that seems to get all the good listings? Actually, depending on your strategy, having one dominant brokerage in your city can be an opportunity for you to give consumers another choice. You just need to decide how you are going to differentiate yourself from the competition.

2. Marketing

Try to find as many examples of your competitors’ branding that you can across multiple platforms like print, social media, online, and events. What are they doing right? What can your new brokerage do better or differently?

3. Branding

Do the successful brokerages in your area have dated brands that don’t line up with the demographics of the area? What kind of brand is doing well in similar cities that’s missing in your city? It can be helpful to think outside real estate here. Think of it as your chance to innovate and create something new for the real estate industry.

4. Brokerage Models

Are there any high-split brokerages? What about virtual brokerages? iBuyers? Flat fee? New agent training companies? What is missing in your market?

5. Culture

This one can be tricky, but what kind of office culture do the successful brokerages have? Are they formal and stuffy? Too laid back? What type of agent do you want to attract?

6. Technology

Do local brokerages make agents suffer using antiquated CRMs or transaction management software? What about agent profiles and listing pages? Do they look like they’re from 2003? Most agents want shiny new technology, so this might be something you can offer.

7. Training & Mentoring

Does your competition just take new agents and throw them to the wolves? If not, what kind of training and mentorship do they provide? How can you, as a small boutique broker-owner, improve on their training and mentoring?

Putting It All Together

Next, see how your dream brokerage works in your local market. Does it fill a need for potential clients? How about for agents? If you want a successful real estate brokerage, you’re going to have to appeal to both.

Now we’ll start modifying your dream brokerage into something that can work in your local area and figure out what you need to make it profitable.

4. Start Building Your Brand

Once you think you’ve narrowed your idea down to a brokerage that works in your local area, you need to start building your brand. While your brokerage’s brand can and will evolve over time, having a well-thought-out brand ready to go will help with your business plan, and just might help you get a loan. Banks want to lend money to businesses with a chance of succeeding, and a strong brand is a key part of that success.

Considering that there are entire college degrees built around branding, we can’t really do the topic justice here. So, for brevity’s sake, we’ll run you through the basics, then link out to articles that will help you nail down the specifics when you’re ready to rock.

Here are the core components of any strong brand, roughly in order of importance:

- Your brokerage’s name: The keystone of every great brand: What you name your business is one of the most important decisions you’ll make. That said, it doesn’t have to be rocket science. If you want to learn more about coming up with a name that will help your brokerage thrive, check out our in-depth guide to naming a real estate business here.

- Your brokerage’s logo: After your name, your brokerage’s logo is the second-most important element of your brand. After all, your logo is a visual representation of everything your brand stands for. You owe it to yourself to create a professional logo. To learn more, check out our guide to great real estate logos here.

- Your brokerage’s slogan: A memorable slogan, also known as a tagline (“Think Different”), can also help get more leads and close more deals. If you want to learn more about writing great slogans, check out our in-depth guide to real estate slogans here.

Real Estate Branding: How to Build Your Brand (+ Case Studies)

Start Claiming Your Online Real Estate

Once you’ve settled on a good brand, the next step is to make sure you can actually use it online. Now go try to claim a domain name and social media accounts with your name. If you’re using your last name in your brand, this part will be easy. If you’re using relatively common words in your brand, finding available domain names and social media accounts might be an expensive challenge, so choose wisely.

5. Draft a Business Plan for Your Brokerage

Once you’ve created a brand that you can work with, the next step will be to create a business plan for your real estate business. While this task might seem daunting, it’s one of the most important documents you’ll ever write for your business, so take it seriously.

Here’s a quick rundown of what to include in your business plan.

An Executive Summary

An executive summary on a business plan is where you briefly outline your path to success. How do you plan to fund your brokerage? How will you recruit agents? What will you pay them? Why does your local area need a new brokerage?

A Financial Plan

Next, you’re going to need to break out the calculator and make sure your numbers really do add up. Here are a few ideas to think about including in your financial plan so that anyone can see a clear path to profitability for your business:

Your Splits & Fees Model

What do you plan to pay your agents? A high split might get more experienced bodies through the door, but you’ll have to close a large number of deals per month in order to break even.

If you pay something close to the market rate of 50%, you might have a harder time attracting talented experienced agents, but will get plenty of trainable agents who only have to close a few deals to get you to break even.

Most brokerages tend to go with something right in the middle. High splits and low or no desk fees for experienced agents, and standard splits or even commission shares for newer agents with no experience.

[Related article: The Best Splits & Fees to Charge Your Agents]

Services You Will Offer Agents (e.g., Marketing, Transaction Management)

Today’s agents expect much more from a brokerage than just a good split and low fees. That means it’s crucial to offer compelling services to attract top agents. Services like marketing, printing, sign installation, inside sales agents (ISAs), and transaction management will all help you attract agents, so they need to be spelled out in your business plan.

[Related article: 9 Services Smart Brokerages Are Offering to Attract More Agents]

An Office Plan: Brick & Mortar vs Virtual vs Coworking

Do you plan to rent out local office space or build a virtual brokerage? If you want to go virtual, then you can cross off rent as an expense and possibly offer better splits and get more talented agents. On the other hand, renting a nice local office goes a long way toward establishing trust with your potential clients.

[Related article: How to Select the Right Office for Your Real Estate Brokerage]

A Lead Generation Plan

To keep your agents happy, how do you plan to get them lots of leads to work? Again, there are a ton of options here, but Zillow and SmartZip keep coming back as the best lead sources for new brokerages. Zillow has amazing brokerage features and offers sophisticated ways to generate buy and seller leads. SmartZip uses artificial intelligence to instantly sift through hundreds of data points on the internet and your MLS with one goal: to find homeowners who are getting ready to sell—before they contact their first agent. Check if you zip code is available.

If you have limited cash on hand, spending it on lead generation might be your best bet for the first year or two. While technology is great, nothing is more attractive for agents than leads.

Here’s James McGrath, co-founder of Manhattan brokerage Yoreevo, on the importance of offering your agents leads:

“For all the talk of technology (e.g., Compass), I don’t see anything on the horizon that agents will care about. The reality is agents spend very little of their time actually working with clients, so making that part of the job more efficient isn’t the point. By generating leads, we make sure our agents are spending more of their time with clients—that’s a difference-maker.”

James McGrath, co-founder of Yoreevo

Still not convinced? Check out our interview with Kendrick Realty founder Luke Monroe on why he spends a whopping $155,000 per month on leads for his agents.

Your Agent Recruitment Plan

Believe it or not, even in crowded cities like New York, recruiting new agents and getting them to stay with you can be a full-time job. How much money, time, and effort do you plan on investing in recruiting new agents? How and where do you plan to recruit?

As an aside, many new broker-owners are afraid to start a brokerage because they don’t think they can woo top talent away from the big players.

While this is a concern you need to plan ahead to mitigate, don’t worry too much about it. You can still build a highly profitable brokerage with a mix of new and mid-level agents.

[Related article: The Ultimate Guide to Recruiting Agents for Your Team or Brokerage]

[Related article: How to Attract the Agents Who Will Help Your Brokerage Grow]

A Technology (CRM, Websites, Transaction Management, VoIP) Plan

What kind of technology can you offer your new agents without breaking the bank? In most cases, the more high-end the software you offer agents, the more agents you’ll attract. As an added bonus, many agents will be far more effective using advanced CRMs, like Propertybase, that can automate outreach and follow-up.

Voice-over-internet-protocol (VoIP) is another way to attract agents and let them work smarter instead of harder. VoIP companies like Grasshopper offer multiple lines for cell phones as well as scalable, advanced VoIP phone systems for brick-and-mortar offices.

Here’s Eric Stegemann, CEO of website and tech provider Tribus, on the importance of providing technology that can scale along with your brokerage:

“While technology like a great CRM is crucial these days, don’t sweat it if you don’t have a ton of money to spend on the latest and greatest technology. The odds of you competing with franchises that spend millions on in-house tech are slim anyway. Instead, focus on the value you can offer.”

[Related article: Real Estate Brokerage Software: 27 Essential Tools]

Management Structure

One of the most neglected elements of running a successful real estate brokerage is management. Most new broker-owners end up micromanaging their new agents or worse, taking a laissez-faire approach, which can end up in litigation.

As you might imagine, supervision can be more of a problem for virtual offices, especially those where managing brokers also work their own deals.

Here’s attorney and real estate broker James S. Tupitza on the importance of quality control for small, tech-focused brokerages:

“There is an exponential increase in the risk brokers assume as the sales teams move away from the traditional office. Supervision must keep up with all the changes in the way salespersons operate.

“As an aside, I already have one policy limit ($1M) settlement this year against a broker for negligent supervision of a salesperson. I expect a second policy limit settlement in the next few months in another case.”

James S. Tupitza

So before you start signing leases and writing ZipRecruiter ads, figure out exactly how you plan to manage your agents. How will you ensure compliance without being an overbearing tyrant? For most people, the answer will lie in building an organizational chart that spells out each partner’s responsibility and sticking to it.

Technology, especially in transaction management, can also make compliance much, much easier to handle.

A Processes & Procedures Plan

If you think you can just wing it and come up with processes and procedures for your brokerage on the fly, you’re in for a rude awakening. Smart business owners spell out ALL the processes and procedures they will have their agents and employees follow. Good agents do not thrive in chaos. Structure is crucial, even for something as trivial as buying coffee for the office.

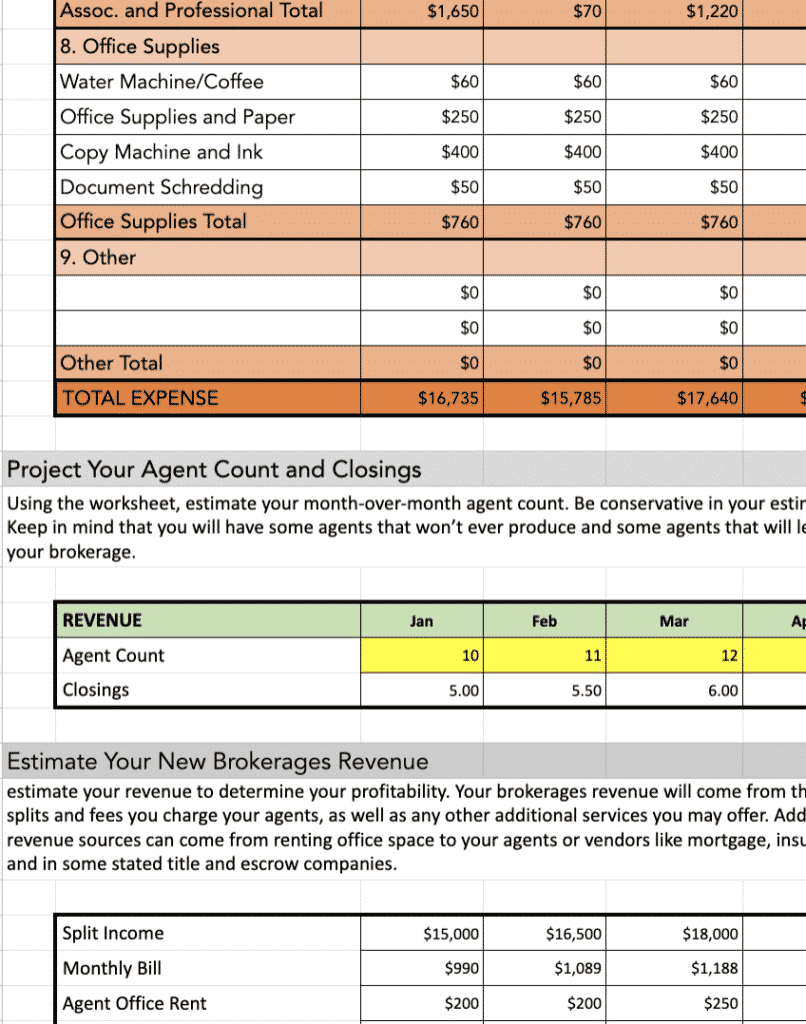

6 Steps to Creating a Real Estate Brokerage Budget in 2022 (+ Worksheet)

A Prospective Budget

In the budgeting section of your business plan, you’re going to take all of your hopes and dreams for your brokerage and (hopefully) make the numbers work.

Of course, your budget won’t be an exact representation of your monthly expenses, but it’s a good starting point to estimate how many agents you’ll need and how many deals they’ll need to close to break even, or better yet, make a profit.

Let’s go through a quick hypothetical budget so you can get an idea of the types of quarterly expenses and revenue estimates you might need to include.

Support Staff Hiring Plan

A brokerage without support staff is basically dead in the water in 2022. At a minimum, you will likely need to hire a receptionist and a transaction coordinator. If you’re serious about marketing, a marketing manager too.

[Related article: The 5 Employees You Need to Hire to Grow Your Brokerage]

Quarterly Expenses

- Office space: $6,000

- Utilities: $750

- Recruitment: $900

- E&O insurance: $190 x 10 agents = $1,900

- Lead generation: $4,500

- Employee salaries: $18,750

- Marketing expenses: $3,000

- Loan repayment: $3,000

Total Expenses: $38,800

Target Quarterly Revenue

- Median listing price: $500,000

- Gross commission income per deal: $15,000

- Agent split: -$7,500

- Total revenue per deal closed: $7,500

- x 7 agents closing two deals per quarter: $104,000

- Quarterly expenses: -$38,800

Total Quarterly Revenue: $65,900

Keep in mind this is a highly simplified budget and does not factor in slow seasons or agent turnover and training.

Whatever you do, try to look at your revenue projections as soberly and honestly as possible. Being confident in your abilities is great, but the realities of the market have ended many would-be brokerages before they even really got off the ground. Don’t make that mistake.

6. Secure Financing & Office Space

Now that you’ve come up with a bulletproof business plan, it’s time to secure your financing and start looking for office space.

With the budget you came up with earlier, figure out how much money you’ll need to keep the business afloat for at least two to six months with no revenue. Keep in mind that this is in addition to having a similar personal financial cushion. This is just to keep your lights on should things suddenly turn pear-shaped.

Where to Get Financing for Your Real Estate Business

Financing a real estate brokerage can be tricky. Real estate brokerages don’t have large assets to lend against—only desks and a few computers. That means the banks don’t have any security. Instead, they will probably make you secure the loan with your personal assets (SBA does this). This makes taking a loan out very risky.

You can get an SBA loan that allows you to use money from your 401(k) to start a business, get a traditional bank loan, use your own cash or a relative’s, or more than likely some combination of all three. Just be aware that you will likely need to secure your loans with personal assets.

Cover Your Bases Legally

If you have partners, you also need to make sure you have all agreed-upon shares of revenues and are all jointly and severally liable for any and all expenses or potential losses. A limited liability company (LLC) is probably your best bet here, but make sure to consult with a lawyer to see what might work best for your unique circumstances.

How to Find & Lease Office Space for Your New Brokerage

Finding a physical home for your new brokerage is one of the trickiest parts of getting started. In most cities worth working in, good office space is a hot commodity, and therefore very expensive. Good retail space is even more expensive. Here are a few tips to help you find a space that works.

Start Small

Since commercial leases are long and your growth doesn’t come with guarantees, don’t lease a giant space right off the bat or make personal guarantees. Instead, consider co-working spaces, or subleasing space in larger offices that already have things like dedicated phone lines, conference rooms, and fast, dedicated internet connections.

Pay Attention to Aesthetics

While the whole plucky garage-based startup thing might score you some points with the Gary Vee crowd on Instagram, your customers won’t see it that way. Instead, they’re going to think twice about your professionalism. So make sure whatever space you rent is well-furnished and pleasant.

Choose a Location That Works for Your Agents & Your Customers

If your agents have to commute 20 miles to your office every day, then chances are they aren’t going to stick around. Likewise, if they have to drive half an hour to each showing. So choose a location that is convenient for your agents and ideally offers some foot traffic to draw in customers.

7. Start Recruiting New Agents

Yes, you’ve done a lot of work to get to this point, but don’t pat yourself on the back just yet. Now you need to start what will become one of the most time-consuming and often frustrating parts of running a brokerage. Recruiting—and more importantly—keeping talented agents who will actually close deals.

As a rule, buyer’s agents will be a whole lot easier to recruit than listing agents, but just keep in mind that you’re probably going to have to feed your new buyer’s agents leads, or have an aggressive sales training program to help them get leads quickly. Most new buyer’s agents have limited marketing resources and few connections but will be hungry enough to close deals for you.

Try to get a decent mix of buyer’s agents and listing agents if you can. Recruiting listing agents won’t be easy, but investing the time, effort, and money into recruiting them will be worth it. Every new listing agent you can recruit helps you build your brand.

How to Recruit Talented Agents Without Resorting to Begging

Well, we hate to say it, but one of the best ways to get great agents on your team is to steal them. That’s right. Being mindful of non-compete clauses in previous contracts, get ready to start wooing talent away from dull, old competitors. After all, you’re the cool new kid on the block and their curiosity will never be higher than right now.

The hard part, of course, is getting talented people in the door without losing your shirt offering high splits, signing bonuses, or other perks. That said, if you can make the math work, then go for it. Paying a top-producing listing agent a $10,000 bonus to come on at a 70% split could end up paying your quarterly expenses with one big deal. A one-year return on your investment is a good rule of thumb. If you spend $10,000 to acquire an agent, you need to get that back in the first year.

Recruiting agents is not easy. Even market-dominating brokerages like Compass have to woo top-producing agents from other firms with perks like signing bonuses, marketing budgets, or even splits that mean they will see little profit from these agents. The business that a top producer can bring to your brokerage means other agents will take notice and recruiting will become that much easier.

Make Sure the Agents You Recruit Are a Good Cultural Fit

Since agents seem to switch brokerages as often as they change their socks these days, retaining agents once you’ve managed to recruit them will be an ongoing battle. Remember, they left their previous broker to come work for you!

This is why screening for a good cultural fit is crucial to hiring agents who will stay for the long haul.

“Know your people. Agents will want to join you—be sure they value what you offer.”

By cultural fit, I don’t mean that you like the same kinds of TV shows or root for the same baseball team. While that can help keep agents around too, in this case cultural fit refers more to your corporate culture and values you worked out in the first step of this guide. For example, does your new recruit share your philosophy of customer service? Are they willing to let a deal slip away to do the right thing?

Over to You

Have great advice for starting a real estate brokerage in 2022 and a burning desire to share with 100,000 other agents? Let us know in the comments!